Diesel engine availability is the single most critical variable in freight transport reliability. Over 97% of Class 8 trucks in North America run on diesel, making it the operational backbone of every major supply chain. When diesel engines are scarce, whether through fuel shortages, parts failures, or fleet downtime, the entire freight network feels the pressure. Understanding why diesel engine availability matters in logistics is not optional for fleet managers. It is the foundation of every capacity, cost, and delivery decision you make.

Why diesel engine availability matters in logistics operations

Diesel engines dominate freight transport because of physics, not preference. Diesel fuel contains roughly 15% more energy per gallon than gasoline. That energy density translates directly into fewer fuel stops, longer hauls, and lower cost per ton-mile on routes that gasoline or electric powertrains simply cannot match.

The performance gap is significant. Diesel engines deliver 30–35% better fuel economy than gasoline equivalents and last 3–4 times longer under heavy-duty conditions. A well-maintained diesel engine supports 100,000–150,000 miles per year. That durability directly reduces replacement frequency and total fleet ownership cost.

Torque is the other factor logistics professionals often underestimate. Diesel engines generate maximum torque at low RPM. That characteristic matters when you are pulling 80,000 pounds up a grade in the Appalachians or navigating a loaded flatbed through mountain corridors in the Rockies. Gasoline engines cannot replicate that low-end pulling power at scale.

Here is how diesel compares to the main alternatives on the metrics that matter most to fleet managers:

| Metric | Diesel | Gasoline | Battery Electric |

|---|---|---|---|

| Fuel economy (Class 8) | Up to 11.8 mpg | 6–8 mpg | Equivalent range limited |

| Engine lifespan | 3–4x longer | Baseline | Battery degradation risk |

| Low-end torque | Excellent | Moderate | Good (instant torque) |

| Refueling infrastructure | Nationwide | Nationwide | Limited for heavy trucks |

| Long-haul viability | High | Low | Currently limited |

Pro Tip: Track your fleet's actual cost per ton-mile quarterly, not just fuel cost per gallon. Diesel's fuel economy advantage compounds over long hauls and shows up clearly in that metric.

How does diesel scarcity disrupt supply chain reliability?

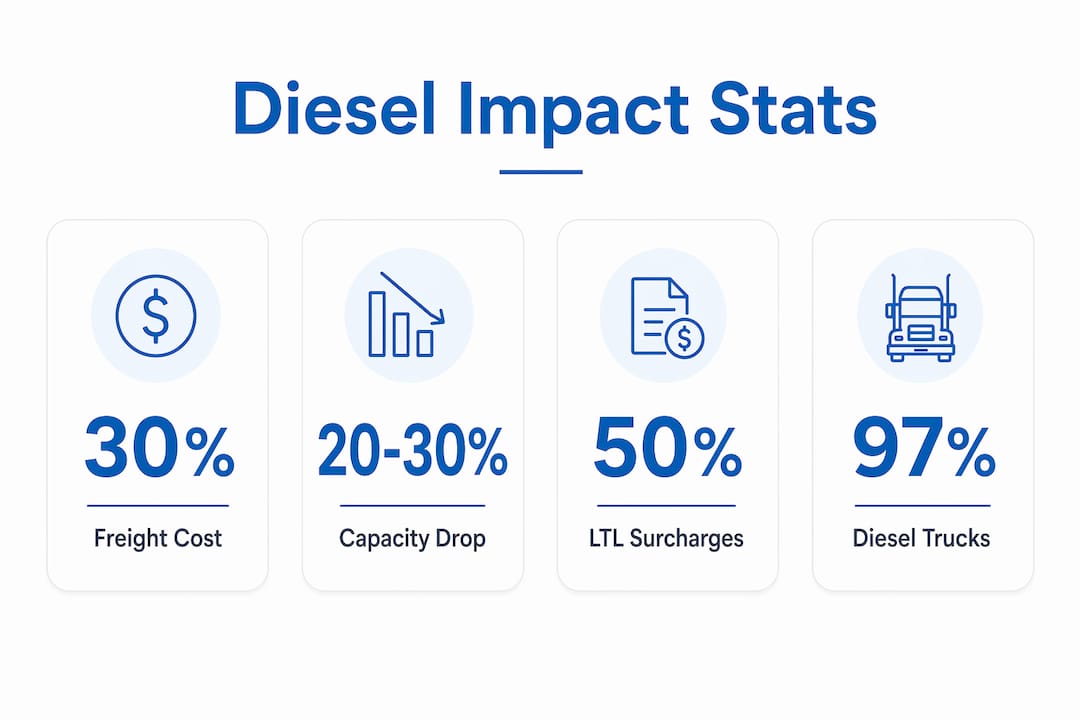

The impact of diesel availability on supply chain performance became impossible to ignore in 2026. U.S. distillate inventories dropped below 103 million barrels in May 2026, pushing diesel prices above $5.37 per gallon. That was not just a fuel cost problem. It was a capacity problem.

Regional rationing followed the inventory drop. Carriers in affected corridors reported capacity drops of 20–30% and delivery delays of 2–5 days. Those numbers sound manageable in isolation. They are not manageable when your customer is a grocery distributor or an automotive assembly plant running just-in-time inventory.

The freight cost effects were severe. Spot freight costs rose nearly 30% during the disruption, and LTL surcharges climbed approximately 50%. Those surcharges hit shippers who lacked long-term carrier contracts hardest. The lesson is direct: spot market dependency becomes extremely expensive when diesel supply tightens.

The cascade effect is what separates diesel scarcity from other cost pressures. Independent operators drop routes first when fuel becomes scarce or unaffordable. That creates localized capacity vacuums in specific corridors, not uniform national shortages. A shipper in the Gulf Coast or Southeast may face acute capacity loss while a shipper in the Midwest experiences only mild disruption. That geographic unevenness makes planning harder, not easier.

What risk management strategies work for diesel volatility?

Industry analysts now treat diesel volatility as a permanent strategic risk, not a cyclical inconvenience. That framing change matters. If you budget for diesel as a stable input, you will be caught unprepared when the next shortage hits. If you treat it as a variable risk, you build contingency into your operations before you need it.

Here is a practical framework for managing diesel availability risk:

- Stress-test your network for a 20–30% carrier capacity drop. Simulating realistic shortage conditions reveals which lanes and customers are most exposed. Run this exercise annually, not after a crisis starts.

- Diversify your carrier base across fuel types and contract structures. Relying on a single carrier or a spot-heavy mix leaves you exposed. Maintain contracted capacity with at least two carriers per critical lane.

- Negotiate priority fuel access agreements with distributors. Diesel scarcity causes route drops by independent operators first. Carriers with guaranteed fuel access maintain routes longer. Ask your carriers directly whether they hold supply agreements.

- Build fuel surcharge clauses into all customer contracts. Transparent surcharge language prevents margin erosion and reduces disputes when prices spike. Index the clause to a published benchmark like the U.S. Energy Information Administration weekly retail diesel price.

- Apply driver coaching and load optimization programs. Advanced driver coaching and load optimization can yield 5–10% fuel economy improvements on existing diesel fleets. That buffer reduces your exposure to price spikes without requiring capital investment.

Pro Tip: Coordinate warehouse receiving windows with your carriers during shortage periods. Reducing driver wait times at docks cuts idle fuel consumption and keeps your lanes more attractive to carriers managing tight fuel budgets.

Diesel vs. electric and hydrogen: which wins for freight?

Diesel remains the operational benchmark for heavy freight because of its mature infrastructure and operational flexibility. Battery electric vehicles and hydrogen fuel cell trucks are real technologies. They are not yet practical replacements for long-haul Class 8 operations at scale.

The infrastructure gap is the core issue. Diesel fueling infrastructure covers every major freight corridor in the United States. Battery electric charging infrastructure for heavy trucks is concentrated in California and a handful of urban markets. Hydrogen fueling stations for Class 8 trucks are even more limited. A fleet manager running lanes from Memphis to Chicago or Dallas to Denver cannot build a reliable schedule around charging infrastructure that does not yet exist along those routes.

Range and terrain add further constraints. Battery electric trucks perform well on predictable urban and regional routes with moderate loads. They face real limitations on mountainous terrain, in extreme cold, and on routes exceeding 300 miles without charging. Those are not edge cases in freight logistics. They describe a large share of actual U.S. freight volume.

| Factor | Diesel | Battery Electric | Hydrogen |

|---|---|---|---|

| Infrastructure maturity | Nationwide | Limited corridors | Very limited |

| Range (Class 8) | 1,000+ miles | 150–300 miles | 300–500 miles |

| Cold weather performance | Reliable | Reduced range | Moderate |

| Refuel/recharge time | 10–15 minutes | 1–4 hours | 15–30 minutes |

| Fleet transition cost | Low (existing fleet) | High | Very high |

This does not mean ignoring alternative powertrains in your fleet planning. It means being honest about the timeline. Diesel will remain the primary power source for long-haul freight through the next decade. Fleet transition planning should account for that reality rather than chase a timeline that infrastructure cannot support.

How to optimize fleet performance amid diesel constraints

Operational discipline is the most underused tool in logistics efficiency. Most fleet managers focus on procurement and contracts. The bigger gains often come from how you operate the assets you already have.

Real-time market monitoring and diversified supply arrangements are the foundation of network stability during diesel disruptions. Panic-driven responses, such as bulk spot purchasing at peak prices or sudden carrier switches, consistently make disruptions worse. Coordinated, pre-planned responses preserve capacity and cost structure.

Specific steps that deliver measurable results:

- Monitor the U.S. Energy Information Administration weekly diesel inventory reports. Set internal alerts when distillate stocks fall below 110 million barrels. That threshold gives you 2–3 weeks of lead time before regional shortages typically emerge.

- Build delivery optimization practices into your standard operating procedures. Consolidating shipments, reducing empty miles, and tightening load factors all reduce fuel consumption per unit delivered.

- Engage suppliers and customers early when you see supply signals tightening. Transparent communication prevents the panic ordering and double-booking that amplifies shortages.

- Review your freight logistics strategies annually against current diesel market conditions. A strategy built in a $3.50 per gallon environment needs adjustment in a $5.37 per gallon environment.

The fleet managers who navigate diesel volatility best are not the ones with the lowest fuel costs in normal times. They are the ones with the most stable capacity and delivery performance during disruptions.

Key takeaways

Diesel engine availability is a structural logistics risk that requires proactive management, not reactive cost control.

| Point | Details |

|---|---|

| Diesel dominates freight | Over 97% of Class 8 trucks run on diesel due to superior fuel economy and durability. |

| Scarcity creates cascade failures | Inventory lows in 2026 caused 20–30% capacity drops and delivery delays of 2–5 days. |

| Cost spikes are severe | Spot freight costs rose nearly 30% and LTL surcharges climbed 50% during May 2026 shortages. |

| Risk management is non-negotiable | Treat diesel volatility as a permanent strategic risk and stress-test your network annually. |

| Diesel alternatives are not ready | Electric and hydrogen trucks face range and infrastructure limits that make diesel irreplaceable for long-haul freight through the next decade. |

The uncomfortable truth about diesel dependency

I have spent years watching logistics professionals treat diesel as a commodity input, something you budget for and move on. That mindset works fine when supply is stable. It fails badly when it is not.

The May 2026 shortage was not a black swan event. Distillate inventories had been trending lower for months before prices crossed $5.37 per gallon. The signals were there. Most operators were not watching them. The ones who had priority fuel agreements and diversified carrier contracts kept their networks running. The ones who relied on spot capacity and assumed diesel would always be available scrambled to explain delays to their customers.

My honest view is that diesel volatility has permanently changed the calculus of supply chain design. You cannot separate fuel strategy from network strategy anymore. The fleet managers I respect most are the ones who treat their Cummins diesel engines and Detroit Diesel assets as strategic infrastructure, not just rolling equipment. They maintain those assets aggressively, monitor fuel markets continuously, and build operational flexibility into every contract.

The alternative powertrains will matter eventually. But eventually is not now. Build your strategy around the infrastructure that exists, not the infrastructure that is promised.

— Carl

Keep your diesel fleet running with Nationwideheavytruckparts

When diesel engine availability tightens across the market, the last thing you need is a fleet sitting idle because of a failed engine. Nationwideheavytruckparts stocks a daily-changing inventory of tested and inspected commercial truck engines, including CAT engines, Mack, Detroit Diesel, and Cummins units, all backed by a standard warranty.

Every part is inspected before it ships. Same-day shipping keeps your trucks moving when downtime is not an option. Whether you manage five trucks or five hundred, Nationwideheavytruckparts gives you fast access to the commercial truck engines your fleet depends on. Do not let an engine failure turn a fuel shortage into a full operational crisis.

FAQ

Why do over 97% of class 8 trucks use diesel engines?

Diesel engines provide 30–35% better fuel economy than gasoline and last 3–4 times longer under heavy-duty conditions. Those advantages make diesel the only practical powertrain for long-haul freight at commercial scale.

How does diesel scarcity affect freight costs?

During the May 2026 shortage, spot freight costs rose nearly 30% and LTL surcharges climbed approximately 50%. Shippers without long-term carrier contracts absorbed the full impact of those increases.

What is the best way to manage diesel availability risk?

Treat diesel volatility as a permanent strategic risk by diversifying your carrier base, negotiating priority fuel access agreements, and stress-testing your network for 20–30% capacity drops before a shortage occurs.

Can electric trucks replace diesel in long-haul logistics now?

Battery electric Class 8 trucks currently face range limits of 150–300 miles and limited charging infrastructure outside California. Diesel remains the only viable option for most long-haul freight corridors in the United States today.

How much fuel economy improvement can driver coaching deliver?

Advanced driver coaching combined with load optimization can yield 5–10% fuel economy improvements on existing diesel fleets, reducing both fuel cost and exposure to price volatility without capital investment in new equipment.